Economics Micro questions from CUET UG 2025.

A consumer derives 10 utilities of satisfaction from consuming 1st unit of good X and 6 utilities of satisfaction from the next unit. What is the marginal utility of the second unit?

A consumer is willing to give up 4 bananas if it is given an extra mango, but in the market, if it gives up 6 bananas, this bundle will be considered.

A consumer spends all his income of Rs 6000 on two goods - Food and clothing and is buying 12 units each of both the goods. At the present level of consumption, the marginal rate of substitution of clothing for food is 3. The price of food per unit is Rs. 400 whereas that of clothing is Rs. 100. What should a consumer do to attain the equilibrium?

A firm increased the capital by a unit, which led to a rise in total product from 10 units to 24 units. Further increase in capital in the same quantity leads to an increase in total product to 40 units. What is the difference in change in marginal product? 1. 14 2. 2 3. 30 4. 16

A firm is operating in a market where it can sell more only by lowering the price of the good. Arrange the changes in total revenue of this firm in a sequential order. (A) Total revenue falls. (B) Total revenue starts from origin. (C) Total revenue increases at a diminishing rate. (D) Total revenue reaches its maximum. Choose the correct answer from the options given below:

A firm produce $q$ amount of output using $x₁$ amount of factor 1 and $x₂$ amount of factor 2. Match List-I with List-II | List-I | List-II | |--------|---------| | (A). Cobb-Douglas Production Function | (I). $f(tx_1, tx_2) > t \cdot f(x_1, x_2)$ | | (B). Constant returns to scale | (II). $f(tx_1, tx_2) < t \cdot f(x_1, x_2)$ | | (C). Increasing returns to scale | (III). $q = x_1^\alpha x_2^\beta$ | | (D). Decreasing returns to scale | (IV). $f(tx_1, tx_2) = t \cdot f(x_1, x_2)$ | Choose the correct answer from the options given below:

A firm will shut down in the short run if__________.

A firm wishes to maximize its profit, find the correct conditions from the following, that must be held by the firm at q₂ at which its profit is maximum. (A) The price must be less than the average variable cost (B) The price must be greater than the average variable cost (C) Marginal cost must be non-decreasing (D) The price, p, must equal MC Choose the correct answer from the options given below:

A functional relation between the two variables expressed $y = 50 - x$, will have slope.

A hurricane in some parts of the country destroyed a major part of the onion crop. Arrange the chain effects of the same on onion market in proper sequence. (A) There will be upward pressure on the price of onions. (B) The buyers will compete in order to get onions in the market. (C) Demand contracts and supply expands until the market achieves a new equilibrium. (D) The market supply of onions decreases, leading to excess demand for the same. Choose the correct answer from the options given below:

A market where firms can choose where to locate production and workers can choose where to work is called?

A perfectly competitive market in an economy is categorized by the following features. (A) Firms are price-takers. (B) Average revenue is equal to market price. (C) Market is perfectly inelastic. (D) Marginal revenue is equal to market price. Choose the correct answer from the options given below:

A point outside the Production Possibility Curve represents: 1. A combination of goods can be produced but resources are underutilized. 2. A combination of goods can be produced, and the resources are fully utilized. 3. A combination of goods can not be produced as it is beyond the capacity of the economy. 4. A combination of goods can be produced and resources are appropriately utilized.

A profit-maximizing firm will attain its equilibrium at that level of output where?

A rational consumer reaches to equilibrium when:

A set of arrangements where economic agents can freely exchange their endowments or products with each other. Such an economy is defined as?

A shift in the budget line, when prices are constant, is due to.

According to the law of variable proportions, the marginal product of an input initially rises and then after a certain level of employment, it starts falling. The MP curve therefore looks like:

According to the law of variable proportions. Which among the the following option is correct?

An economy has to choose one of the many possibilities that it has at given resources. Therefore, the cost that an additional unit of X commodity in terms of the amount of the Y commodity that has to be forgone is called ................ cost.

An increase in production of one extra unit of output will lead to an increase in ..........

An increase in the price of socks is likely to decrease the demand for shoes and a decrease in the price of socks is likely to increase the demand for shoes. Socks and shoes are:

An individual buys $15$ kg of sugar when its price is Rs. $5$ per kg. When the price increases to Rs. $7$ per kg, the demand goes down to $12$ kg of sugar. What is the price elasticity of demand for sugar?

An institution which organizes the free interaction of individuals pursuing their respective economic activities, is known as...........

An upward sloping straight line supply curve shooting from the X axis indicates the:

Anand consumes lesser units of good X when its price falls but more units of X when his income rises. Which of the following statements is true about good X.

Any allocation of resources by the society would result in the _____ of a particular combination of different goods and services.

Arrange a statement of market equilibrium when the demand curve shifts leftward: (A). The shift indicates that at any price the quantity demanded is less than before. (B). Some firms will reduce the price of their commodity so that they can sell their desired quantity. (C). Excess supply will arise. (D). At the new equilibrium, quantity and price will be less than before. Choose the correct answer from the options given below:

Arrange the following concept emerges in context of consumer equilibrium. (A) Transfer his expenditure from Good Y to Good X. (B) Sacrifice more of Good Y to gain Good X. (C) Till, Marginal Rate of Substitution (MRSxy) = Market Rate of Exchnage. (D) Suppose, Marginal Rate of Substitution (MRSxy) > Market Rate of Exchnage. Choose the correct answer from the options given below:

Arrange the following elasticity degrees along the demand curve in their ascending order. (A) Elasticity (eD) = 1 (B) Elasticity (eD) > 1 (C) Elasticity (eD) < 1 (D) Elasticity (eD) = 0 Choose the correct answer from the options given below:

Arrange the following in correct sequence to attain equilibrium under perfect competition. (A) LRMC start rising. (B) Both LRAC and LRMC fall. (C) Both LRAC and LRMC rises. (D) LRMC cuts LRAC from below.

Arrange the following in correct sequence, to correct the problem of mismatch between supply and demand forces: (A) There is excess demand in the market. (B) All other things remain the same as price rises, quantity demanded falls and quantity supplied increases. (C) Some consumers who are either unable to obtain the commodity at all or obtain it in insufficient quantity will be willing to pay more than the prevailing prices. (D) The market moves towards the point where the quantity that the firms want to sell is equal to the quantity that the consumers want to buy. Choose the correct answer from the options given below:

Arrange the following money supply measures in chronological order. (A) Excess supply will prevail in the economy. (B) The tendency of prices to change to restore equilibrium. (C) Suppose market supply is greater than market demand at a given price. (D) Hence, the market is not in equilibrium. Choose the correct answer from the options given below:

Arrange the following stages of Consumer's Equilibrium in the correct sequence under the utility analysis (A) Marginal Utility becomes equal to the price of a commodity (B) Marginal utility, derived from a commodity X is greater than Px (C) Increase the consumption of commodity X (D) The consumer reallocates expenditure to maximize satisfaction. Choose the correct answer from the options given below:

Arrange the following statement in the context of elasticity along a linear demand curve (left to right). (A) e_d = 1 (B) e_d > 1 (C) e_d = 0 (D) e_d < 1 Choose the correct answer from the options given below:

Arrange the following statement of government intervention in the form of price control. (A) The government sets floors or minimum prices for these goods and services. (B) A fall in price below a particular level is not desirable. (C) The price charged for a particular good or service is called the price floor. (D) The government imposed a lower limit on the price. Choose the correct answer from the options given below:

Arrange the following statement when the market demand curve shifts rightward with the supply curve remaining unchanged. (A) The shift indicates that at any price the quantity demanded is more than before. (B) Some individuals will be willing to pay higher price and the price would tend to rise. (C) There is excess demand. (D) At the new equilibrium, quantity and price will be greater than before. Choose the correct answer from the options given below:

Arrange the following statements considering the shape of long run marginal costs (LRMC). (A) As output increases, LRAC initially falls (MC < AC). (B) For the first unit of output, both LRMC and LRAC are the same. (C) After a certain point, LRAC rises (MC > AC). (D) LRMC curve is therefore a 'U'-shaped curve. Choose the correct answer from the options given below: 1. (A), (B), (C), (D) 2. (B), (A), (C), (D) 3. (B), (A), (D), (C) 4. (C), (B), (D), (A)

Arrange the following statements in chronological order in respect to the impact of a unit tax on supply: (A) Imposition of unit tax increases the price of commodities. (B) Increased prices will lead to an increase in LRAC and LRMC. (C) The firm's long run supply curve shifts to the left. (D) At any given market price, the firm supplies fewer units of output. Choose the correct answer from the options given below:

Arrange the following statements in chronological sequence about how government intervention in the form of price control has an impact on the market. (A) There will be an excess demand for sugar in the market at that price. (B) Government-imposed upper limit on the price of sugar. (C) Quantity of sugar can be distributed to everyone, through a system of rationing. (D) It could end up creating a shortage of sugar in the market. Choose the correct answer from the options given below:

Arrange the following statements in the context of "U" shaped SAC curve. (A) SAC is the sum of AVC and AFC. (B) SAC falls when AVC and AFC decrease. (C) When the fall in AFC is greater than the rise in AVC and SAC is still falling. (D) When a rise in AVC becomes greater than the fall in AFC, SAC rises. Choose the correct answer from the options given below:

Arrange the following statements related to negative externalities in correct sequence (A) There is an oil refinery which refines crude petroleum and sells it in the market (B) Pollution harms well-being and also kills fish or other organisms (C) Production the refinery may also be polluting the nearby river (D) Such harmful effects that the refinery is inflicting on others, for which it will not bear any cost, are called externalities

Arrange the following statements related to the change in demand for normal good. (A) The consumer's income, increases. (B) Given the prices of other goods and the preferences of the consumer, (C) The demand curve shifts rightward. (D) The demand for the normal good at given price changes.

Arrange the following statements showing the change in budget set due to change in income. (A) The equation of the budget line is $P_1 X_1 + P_2 X_2 = M'$. (B) Consumer's income increases from $M$ to $M'$, but the price of goods remains constant. (C) The set of available bundles depends upon prices and the income of the consumer. (D) Consumers can buy more of the goods at the prevailing market prices. Choose the correct answer from the options given below:

Arrange the following steps of Market Equilibrium under perfect competition in the correct order. (A) Excess of market demand over market supply will cause excess demand situation. (B) Quantity demanded will fall and quantity supplied will rise. (C) The market will move towards the point where the quantity that the firm wants to sell is equal to the quantity that the consumer wants to buy. (D) The market price would tend to increase, due to competition among buyers. Choose the correct answer from the options given below:

Arrange the given statements in chronological order stating the implications of free entry and exit assumptions in a equilibrium market. (A) Supply curve shifts rightward, however demand remains unchanged. (B) At the prevailing market price, each firm is earning a supernormal profit and will attract some new firms. (C) Market prices fall, and supernormal profits are eventually wiped out. (D) All firms in the market are earning normal profit, no more firms will have incentive to enter. Choose the correct answer from the options given below:

Arrange the given statements to show the impact on a firm's supply curve due to its determinants. (A) Organisational innovation allows the firm to use fewer units of inputs. (B) Any factor that affects a firm's marginal cost curve is a determinant of its supply curve. (C) At any given market price, the firm now supplies more units of output. (D) The marginal cost will shift downward. Choose the correct answer from the options given below:

Arrange the stages of price determination in a perfect competition market: (A) Estimate the market demand and supply. (B) Firms adjust production to maximize profit. (C) Equilibrium price is established. (D) Short-run profit attracts new firms. Choose the correct answer from the options given below:

Arrange the statements to define the relationship between elasticity and expenditure of a commodity. (A) The percentage increase in quantity demanded is greater than the percentage decline in the price. (B) The impact on expenditure depends on how responsive the demand for the good is to the price change. (C) The nature of price elasticity of demand is elastic. (D) Expenditure on the goods will increase. Choose the correct answer from the options given below:

Arun spends 200 rupees on good X irrespective of its price whereas Varun buys 10 units of Good X irrespective of its price. The respective values of the price elasticity of demand for Good X for both the consumers is

As long as average cost is falling

As long as decreasing returns to scale operates, as the firm increases output, the average cost must be ................

At a price of ₹8 per unit, the quantity supplied of a commodity is 200 units. If its price elasticity of supply is 1.5, if the price rises to ₹10 per unit, calculate the quantity supplied at the new price?

At the final level of production, a typical firm observed.

At the market price of Rs 10, a firm supplies 200 units of a good. If the market price increases to Rs 30, and the price elasticity of the firm's supply is 2. Then at new price what quantity will be supplied by the firm?

At the minimum point of the long run average cost curve .......... is observed.

At the positive level of output, where a firm's profit is maximized, the following conditions must hold. (A) $p = LRMC$ (B) LRMC is non-decreasing at $q_0$ (C) $p \leq LRAC$ (D) $p \geq$ min. LRAC Choose the correct answer from the options given below:

At the present level of production, the marginal revenue exceeds the marginal cost of production. In order to attain equilibrium, the producer should___

At zero level of output ,if the total cost(TC) is 20. What will be the value of the Average Fixed cost (AFC) at the 6th level of output?

Average Fixed Cost (AFC) is indicated by?

Average fixed cost curve is actually a ................... curve:

Budget Set is __________

Calculate the short run average cost when total cost is 95 with 9 units of output.

Calculate total cost of production for producing 100 vases ?

Change in total cost per unit of change in output is defined as:

Choose the correct equations in the context of costs. (A) TFC = AFC × quantity (B) LRMC = (TC at $q_n$ units) – (TC at $q_{n-1}$ units) (C) TC = TVC × TFC (D) LRAC = TC/q Choose the correct answer from the options given below:

Choose the correct options with reference to short-run average costs. (A) Average total cost = total cost / quantity of output (B) Average total cost = average variable cost + average fixed cost (C) Average variable cost = average total cost - average fixed cost (D) Average fixed cost = average variable cost - average cost Choose the correct answer from the options given below:

Choose the correct statements considering the relationship between marginal product and average product. (A) Average product and marginal product curve are 'U'shaped. (B) Average product and marginal product curve are inverse 'U'shaped. (C) When the average product increases, the marginal product is greater than the average product. (D) When the average product decreases, the marginal product is less than the average product. Choose the correct answer from the options given below:

Choose the correct statements from the following. (A) The collection of all possible combinations of goods and services that can be produced from a given amount of resources and a given stock of technological knowledge is called the production possibility frontier. (B) Slope of production possibility frontier is called marginal opportunity cost. (C) In positive economic analysis, we study how the different mechanisms function. (D) Scarcity of resources gives rise to the problem of choice.

Choose the correct statements from the options given below in terms of the shapes of the short run cost curves. (A) Average fixed cost curve is a rectangular hyperbola. (B) Total fixed cost is horizontal straight line. (C) Average variable cost is upward sloping. (D) Marginal cost is U shaped. Choose the correct answer from the options given below:

Choose the correct statements in respect of returns to scale. (A) Decreasing returns to scale occur when a proportional increase in all inputs is less than output. (B) Constant returns to scale occur when a proportional increase in all inputs is the same as output. (C) In the long run, factors of production are increased by the same proportion, or factors are scaled up. (D) Increasing returns to scale occur when a proportional increase in all inputs is less than output. Choose the correct answer from the options given below:

Choose the correct statements in the context of the law of diminishing marginal utility (A) States that each successive unit of a commodity provides lower marginal utility. (B) States that each successive unit of a commodity provides higher marginal utility. (C) Explains why demand curves have a negative slope. (D) States that the marginal utility from consuming each additional unit of a commodity declines as its consumption increases, while keeping consumption of other commodities constant. Choose the correct answer from the options given below:

Choose the incorrect option from the following with reference to production in the short run.

Chronologically, arrange the following statements in the context of shape of AP curve. (A) MP starts falling, the AP continues to rise as long as MP remains higher than AP. (B) At the first level of output, the MP and the AP are the same. (C) MP fall sufficiently, its value becomes less than the AP and the AP also falls. (D) MP rises, AP being the average of marginal products, also rises, but rises less than MP. Choose the correct answer from the options given below:

Consider a production function $q = f (x_1, x_2)$ where the firm produces q amount of output using $x_1$ amount of factor 1 and $x_2$ amount of factor 2. Now suppose the firm decides to increase the employment level of both the factors t (t > 1) times. Identify the correct statement from the following.

Consider the production function $q = f(x_1, x_2)$ where the firm produces q amout of output $x_1$ amount of factor 1 and $x_2$ amount of factor 2. The firm decides to increase the employment level of both the factors t (t > 1). Identify the equation for decreasing returns to scale from the following.

Delhi has become the most polluted city in India. Due to this, how will the production possibility curve of Delhi be affected?

Downward movement along the demand curve is caused by _________.

"Economics is the science of wealth". This statement was given by :-

Extension of supply occurs due to change in _________

Find the correct statement/statements. (A) Goods which are consumed together are called complementary goods. (B) The market demand curve can be derived as a vertical summation of the individual demand curves. (C) Price elasticity of demand is a measure of the responsiveness of the demand for a good to changes in its price. (D) If the consumer's preferences change in favor of a good, the demand curve for such a good shifts leftward. Choose the correct answer from the options given below:

Find the equilibrium price of salt in this market.

Firms can choose where to locate production and workers to choose where to work. There are various immigration laws which restrict the movement of labour between countries. This market is called...

Floor prices are meant for the welfare of

For a hypothetical firm, the total cost of producing 5 units of a commodity is Rs. 310 and that of producing 8 units is Rs. 850. If the firm has to spend Rs. 50 even when there is no output, what will be the marginal cost of producing the 8th unit?

For a price-taking firm, the market price is equal to marginal revenue and ......

For the firm to continue to produce, in the long run, price must be greater than the average cost (p > AC) and in the short run, price must be greater than the ......

From the following statements about a firm's supply curve, select the correct statements: (A) Technological progress is expected to shift the supply curve of a firm to the right. (B) An increase in input prices is expected to shift the supply curve of a firm to the left. (C) A decrease in input prices is expected to shift the supply curve of a firm to the left. (D) The imposition of a unit tax shifts the supply curve of a firm to the left. Choose the correct answer from the options given below:

From the following which is incorrect with respect to firm's profit maximization in long run? 1. Price = Long Run Marginal Cost 2. LRMC is first decreasing and then increasing 3. Price = Short Run Marginal Cost 4. Price ≥ Long Run Average Variable Cost

From the following which production function exhibits increasing returns to scale?

From which of the following, consumers can choose their consumption bundle?

Given the production function $f(tx_1, tx_2) > tf (x_1, x_2)$, what it exhibit:

Good X and Y are considered to be substitutes by a consumer. He is currently consuming good X. If the price of Good Y decreases, then arrange the following in correct sequence. (A) Demand for Good X decreases. (B) Consumer finds Good Y to be relatively cheaper than Good X. (C) Demand curve for Good X shifts to the left. (D) Consumer shifts from Good X to Good Y. Choose the correct answer from the options given below:

How does an increase in price affect supply?

How does technological progress affect the firms' supply curve?

How government intervention through price control policy will have an impact on the market? (A) The government imposed lower limit on the price that may be charged (B) For certain goods and services, a fall in price below a particular level is not desirable (C) Thereby leading to an excess supply in the market (D) Government needs to buy the surplus at the predetermined price Choose the correct answer from the options given below:

How is the value of the average product calculated in the short-run? 1. By dividing the total product by the number of labor. 2. By dividing the change in total product by the change in labor. 3. By dividing the change in total product by the number of labor. 4. By dividing the total product by the change in labor.

How much of Good X can the consumer consume if she spends her entire income on that good?

How much units of Good Y can the consumer consume if she spends her entire income on that good?

How the revelation of the fact that junk-foods might be injurious to health can affect the Demand Curve of junk-foods.

How will an increase in the consumer's income affect the budget line? 1. Parallel inward shift of budget line. 2. Parallel outwards shift in budget line. 3. The budget line rotates outwards. 4. Budget line rotates and shifts outwards.

How would the decrease in the price of Good-X impact the budget line, when the price of Good-Y and Income remain unchanged? 1. The intercept points of both Good-X and Good-Y will shift outward. 2. The intercept point of Good-X will shift outward and the intercept point of Good-Y will remain unchanged. 3. The intercept point of Good-X will shift inward and the intercept point of Good-Y will remain unchanged. 4. The intercept points of both Good-X and Good-Y will shift inward.

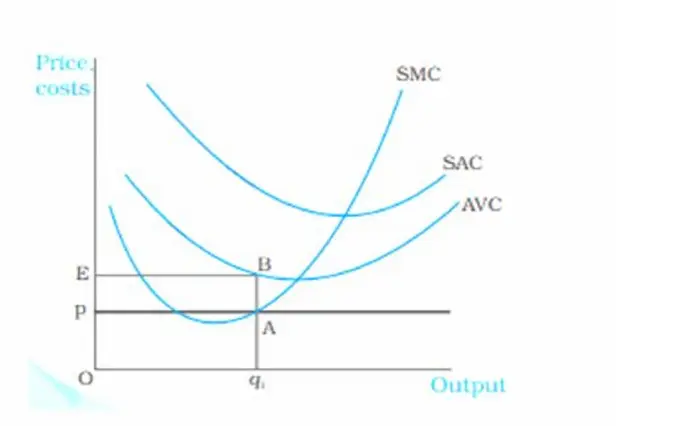

The firm's total variable cost at output q₁ is

Identify the characteristics of the resources from the following (A) Resources are limited (B) Resources are available for free (C) Resources are scarce only in developing countries. (D) Resources have alternative uses. Choose the correct answer from the options given below:

Identify the correct sequence due to which firms under perfect competition earn normal profits in the long run. (A) The firms are earning less than normal profit at the prevailing price. (B) The profits of each firm will increase to the level of normal profit. (C) No more firm will want to leave, since they will be earning normal profit here. (D) Some firms will exit, which will lead to an increase in price. Choose the correct answer from the options given below:

Identify the correct sequence for a firm operating in the short run. (A) Total product increases at a decreasing rate. (B) Marginal product becomes zero (C) Marginal product increases (D) More and more units of variable factor are employed. Choose the correct answer from the options given below:

Identify the correct sequence of events when a minimum support price is imposed: (A) Government buys the surplus at the predetermined price. (B) Situation of Surplus occurs due to imposition of floor price. (C) Government sets a minimum price. (D) Market equilibrium occurs by the intersection of demand and supply curves. Choose the correct answer from the options given below:

Identify the correct sequence to establish the relation between marginal cost and average cost. (A) When Marginal cost falls, average cost also falls. (B) Marginal cost rises but average cost continues to fall. (C) Marginal cost is equal to average cost. (D) Marginal cost rises and average cost also rises. Choose the correct answer from the options given below:

Identify the correct statements from the following: (A) As long as MP>AP, the average Product (AP) can rise even when the Marginal Product (MP) is falling. (B) The law of variable proportions operates only if the factor ratio happens to change. (C) Total Product (TP) must increase no matter if there are increasing or decreasing returns to a factor. (D) Marginal Product (MP) = Average Product (AP), when AP is maximum. Choose the correct answer from the options given below:

Identify the correct statements with regard to the consumer's budget line/set. (A) A decrease in the price of goods makes the budget line steeper (B) A decrease in the price of goods makes the budget line flatter (C) An increase in the price of goods makes the budget line steeper (D) All bundles in the positive quadrant which are on or below the line are included in the budget set.

Identify the factors of price elasticity of demand. (A) Nature of Goods. (B) Availability of Substitution. (C) Complementary Goods (D) Cost of Goods. Choose the correct answer from the options given below:

Identify the incorrect option from the following related to a perfectly competitive market.

Identify the incorrect statement about the relation between Marginal Product(MP) and Average Product (AP).

Identify the incorrect statement regarding price flooring:

Identify the options which reflect the impact of simultaneous shifts of demand and supply on equilibrium (A) When demand shift right and supply left, quantity may increase, decrease or remain unchanged but price decreases (B) When demand and supply shift leftward, quantity decreases but price may increase, decrease or remain unchanged (C) When demand and supply shift rightward, quantity increases but price may increase, decrease or remain unchanged (D) When demand shift left and supply right, quantity may increases, decreases or remain unchanged but price decreases

Identify, where the point will lie in the production possibility frontier when the resources are either underemployed or are utilized in a wasteful manner 1. A point below the production possibility frontier 2. A point above the production possibility frontier 3. A point on the production possibility frontier 4. A point on or above the production possibility frontier

If all the resources are used in the production of cloth, the curve which gives the maximum amount of cloth produced in the economy for any given amount of machine is called?

"If and only if between any two bundles, the consumer prefers the bundle which has more of at least one of the goods and no less of the other good as compared to the other bundle". Such preferences are known as

If demand for salt increases, and there is no change in the equilibrium price in the market, how does it affect the market?

If demand remains constant at any changes in price of commodity then the elasticity of demand for that commodity will be.................... 1. Zero 2. One 3. Between one and zero 4. Infinite

If due to fall in price, total expenditure on the commodity falls, it indicates?

If price of a commodity rises from Rs. 10 to Rs. 15, its supply increases by 20%. calculate the price elasticity of supply for this commodity.

If supply curve shifts leftward and demand curve shifts rightward then how it will affect the pricing?

If the average fixed cost of production is the fixed cost per unit of output produced. Then it will _______.

If the demand for salt increases supply remains the same and the new demand curve is $Q_D = 400 - p$ What will be the new equilibrium price and quantity?

If the government fixed maximum price of product below the market price then product will have?

If the government imposes a price ceiling of Rs 31 on salt, what will be the volume of excess demand/ supply in the market?

If the marginal cost(MC) of a perfectly competitive firm is as given below and the price of the product is Rs 15, find the profit-maximizing output of the firm. | output | 1 | 2 | 3 | 4 | 5 | 6 | |---|---|---|---|---|---|---| | MC | 18 | 15 | 10 | 12 | 15 | 24 |

If the marginal rate of transformation is constant throughout, the production Possibilities Frontier will be

If the price of a commodity increases by 20%, its demand drops by 20%. Then how it will affect the expenditure?

If the price of a good increases from ₹20 to ₹25 and the quantity demanded decreases from 100 units to 80 units, calculate the price elasticity of demand.

If the price of necessity good like clothes changes, what will be the effect on its demand?

If the production is increased to 300 vases, what will happen to Fixed cost per unit?

If the supply curve of a good cuts the price axis in its positive range and as we extend the straight line, it cuts the quantity-axis at its negative range, the elasticity of supply for the good will be:

If the total revenue curve of a firm is an upward sloping straight line, then which of the following is true for this firm?

If there is a positive level of output at which a firm's profit is maximized in the short run, that condition must not hold at that output level:

If we want to have more of one of the goods, we will have less of the other good. Thus, there is always a cost of having a little more of one good in terms of the amount of the other good that has to be forgone. What is this cost known as?

Imposition of price ceilings usually results into?

Imposition of price floors usually lead to following

In a long run average cost curve which point is said to be the constant return to scale?

In a particular country, there was a severe heatwave. Arrange the following in the sequence of order in context of the market of ice-creams. (A) Rise in the price of ice cream. (B) Supply will remain the same. (C) Competition among the buyers of ice cream inceaseees. (D) The demand for ice cream increases. Choose the correct answer from the options given below:

In a perfectly competitive market, a firm produces and sells a certain amount of goods. Among the following what reflect the firm's profit?

In a perfectly competitive market choose the correct statement from the following. (A) Equilibrium occurs where market demand equals market supply. (B) Each firm employs labour upto the point where the marginal revenue of labour equals the wage rate. (C) Equilibrium price and quantity are determined when there is large number of firms. (D) Equilibrium price is always equal to minimum average cost of the firms. Choose the correct answer from the options given below:

In a perfectly competitive market, the marginal revenue curve is?

In a production function $q = f(x_1, x_2)$ where the firm produces q output using $x_1$ of factor 1 and $x_2$ of factor 2. Now suppose the firm decides to increase the employment level of both the factors t (t > 1) times. then which among the following is correct?

In a situation when MRSxy > Px / Py, the consumer would react by:

In an economy producing only two goods X and Y, the opportunity cost of producing 5 units of good X is 3 units of good Y. The above statement implies that _____. (choose the correct option)

In given production function $q = f(x_1, x_2)$ what is depicted by $f(tx_1, tx_2) < tf(x_1, x_2)$.

In inverse 'U'-shaped average product curve; as long as the value of Marginal Product remains higher than the value of the average product, in this condition the average product continues to ..........

In long run as long as average cost is falling, marginal cost must be less than the .......

In Microeconomics, what does supply refer to?

In order to be effective, the price ceiling should be determined _______.

In perfectly competitive market, the demand curve of a firm is?

In the above paragraph, which factor is affecting the supply of Coffee?

In the cardinal utility analysis, the marginal utility of money is considered to be

In the context of perfect competition, which one of the following is not correct?

In the course of production, exchange and consumption of goods and services, every society has to face a scarcity of resources; and it is the scarcity of resources that gives rise to the problem of .............

In the determination of a particular variable, the assumption of "ceteris paribus" stands for.

In the long run, average cost must be rising as the firm increases output as long as the.......... operates.

In the long run __________.

In the long run marginal cost curve shape is ..........

in the long run when the average cost is rising, marginal cost must be.

In the perfectly competitive market, if 10 packets of bread are sold at the price of Rs. 25 per packet, what will be the total revenue of a bread manufacturer? 1. Rs. 25 2. Rs. 250 3. Rs. 0.4 4. Rs. 2.5

In the production of clothes, cotton is defined as................ 1. capital 2. Input. 3. Final Output. 4. Intermediate output

In the short run and long run, the shapes of the cost curves for a typical firm are defined as (A). SMC curve cuts the AVC curve from below at its minimum point. (B). LRAC curve cuts the LRMC curve from below at the minimum point of LRMC. (C). SMC curve cuts the SAC curve from below at the minimum point of SAC. (D). Average fixed cost curve is downward sloping. Choose the correct answer from the options given below:

In the short run, some of the factors of production of a firm ......

In the short run, the shape of marginal cost, average variable cost and short run average cost curves are:

In the short run, the shape of the average fixed cost curve for a typical firm is?

In the short run, which of the following condition is mandatory for a firm for its profit maximization at q₀?

In which condition, the average cost of a firm declines when output increases?

In which of the following conditions, output increases with the same proportion of input?

In which of the following, the demand for a good will be highly price elastic?

Increase in the income of buyers (in case of inferior goods) will cause _________

Individual demand for a good does not depend upon which of the following?

......... is an economy in which there is both the private sector and the government.

Keeping the capital as a fixed input, as 3, when the quantity of labor changes from 3 to 4, the total product with labor also rises from 40 to 50 units. What is the average product after the change? 1. 50 2. 13.33 3. 12.5 4. 40

Lata likes to eat burgers and has already eaten two. Her marginal utility from the last burger she consumes is 90 utils. If the price of burger is Rs. 25 per unit and marginal utility of a rupee is 3 utils, then?

Law of demand is violated when?

Let us consider a linear demand curve $q = a - bp$. On the same demand curve, arrange the elasticity in ascending order. (A) $|e_D| = 1$. (B) $|e_D| < 1$. (C) $|e_D| > 1$. (D) $|e_D| = 0$. Choose the **correct** answer from the options given below:

Let us consider the example of a market consisting of identical farms producing the same quality of wheat. Suppose the market demand curve and the market supply curve for wheat are given by: qᵈ = 200 - p and qˢ = 120 + p. What is the equilibrium price?

LRMC cuts the LRAC curve from below at the point where.

Manoj is a seller in a market where more can be sold only by lowering the price of the goods. Which of the following will be true about his revenue. (A) Total revenue will increase at a constant rate. (B) Average revenue will be more than his marginal revenue at all the levels of output sold. (C) Marginal revenue curve will be downward sloping from left to the right. (D) Marginal revenue can be zero at some level of output sold. Choose the correct answer from the options given below:

Marginal cost curve intersects average cost curve at ..........

Marginal product (MP) and the average product (AP) curves are inverse 'U'-shaped. which of the following is correct for AP and MP.

Match List-I with List-II | Change in Demand or Supply | Effect on equilibrium price / equilibrium quantity | |---|---| | (A) Increase in demand > Increase in supply | (I) equilibrium price will rise but no change in equilibrium quantity. | | (B) Increase in supply when demand is perfectly inelastic | (II) No change in equilibrium price. | | (C) Same proportion of increase in demand and supply | (III) equilibrium price will fall but no change in equilibrium quantity. | | (D) Increase In demand when supply is perfectly inelastic | (IV) equilibrium price and quantity will rise. | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | | --- | --- | | (A) Total revenue | (I) Minimum of LRAC curve. | | (B) Supply | (II) A firm earns only normal profit. | | (C) Shut down point | (III) Market price multiplied by the firm's output. | | (D) Break-even point | (IV) Quantity sold at a given price. | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | | --- | --- | | (A) Payments by a firm for inputs. | (I) Cost of production | | (B) Output sold by a firm in the market. | (II) Revenue | | (C) Inputs are transformed into output. | (III) Production | | (D) Objective of a firm to maximize. | (IV) Profit | Choose the **correct** answer from the options given below:

Match List-I with List-II | List-I | List-II | | --- | --- | | (A) Relationship between the variable input and output. | (I) Average Product | | (B) Output per unit of variable input. | (II) Marginal Product | | (C) Change in output per unit of change in the input | (III) Law of variable proportions | | (D) The marginal product of a factor input initially rises with its employment level | (IV) Total Product | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | | --- | --- | | (A) Analysis assumes that level of utility can be expressed in numbers. | (I) Cardinal Utility | | (B) Change in total utility due to consumption of one additional unit of a commodity | (II) Law of Diminishing Marginal Utility. | | (C) Marginal utility from consuming each additional unit of a commodity declines as its consumption increases. | (III) Marginal Utility | | (D) The amount of mangoes that the consumer has to forego in order to get an additional banana, her total utility level being the same. | (IV) Marginal rate of substitution | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Perfect Competition | (I) A typical characteristic of perfect competition. | | (B) Perfectly elastic demand curve | (II) An individual firm is a price taker. | | (C) Degree of price control under perfect competition | (III) The firm can sell any amount of its output at the prevailing price. | | (D) Freedom of entry and exit | (IV) No control over price. | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Satisfaction derived from consuming the given amount of some commodity x. | (I) Marginal rate of substitution. | | (B) Change in total utility due to consumption of one additional unit of a commodity. | (II) Ordinal Utility | | (C) Ranking of various consumption bundle. | (III) Marginal Utility | | (D) Downward slope of indifference curve. | (IV) Total Utility | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Upper limit on price of goods & services | (I) Leads to excess supply. | | (B) Free entry and exit | (II) Equilibrium price = min AC of the firms. | | (C) Marginal revenue product of labor (MRP_L) | (III) Leads to excess demand. | | (D) Lower limit on price of goods & services | (IV) MR x MP_L. | Choose the correct answer from the options given below: 1. (A) - (I), (B) - (II), (C) - (III), (D) - (IV) 2. (A) - (III), (B) - (II), (C) - (IV), (D) - (I) 3. (A) - (IV), (B) - (III), (C) - (II), (D) - (I) 4. (A) - (IV), (B) - (III), (C) - (I), (D) - (II)

Match List-I with List-II | List-I | List-II | |---|---| | (A) Consumer's equilibrium | (I) ΔY/ ΔX | | (B) Slope of IC | (II) Budget line rotates to the right starting from the Y axis | | (C) Px falls | (III) Consumer should move downwards to the right along the IC | | (D) MRSxy > Px/Py | (IV) Optimum choice of the consumer | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Production function | (I) $f(tx_1, tx_2) > t f(x_1, x_2)$ | | (B) Constant returns to scale | (II) $f(tx_1, tx_2) < t f(x_1, x_2)$ | | (C) Increasing returns to scale | (III) $f(x_1, x_2)$ | | (D) Decreasing returns to scale | (IV) $f(tx_1, tx_2) = t f(x_1, x_2)$ | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Cardinal utility | (I) Ranking consumption bundles. | | (B) Perfect substitute goods | (II) Level of utility can be expressed in numbers. | | (C) Ordinal Utility | (III) The marginal Rate of Substitution is 1. | | (D) Complimentary goods | (IV) An increase in the price of one good does not lead to an increase in demand for another good. | Choose the correct answer from the options given below: 1. (A) - (I), (B) - (IV), (C) - (III), (D) - (II) 2. (A) - (II), (B) - (III), (C) - (I), (D) - (IV) 3. (A) - (I), (B) - (IV), (C) - (II), (D) - (III) 4. (A) - (III), (B) - (IV), (C) - (I), (D) - (II)

Match List-I with List-II | List-I | List-II | |---|---| | (A) Budget Set | (I) $-(P_1/P_2)$ | | (B) Slope of the budget line | (II) $M/P_1$ | | (C) Horizontal intercept of the budget line | (III) $P_1 X_1 + P_2 X_2 \le M$ | | (D) Vertical intercept of the budget line | (IV) $M/P_2$ | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Land | (I) Interest | | (B) Labor | (II) Profit | | (C) Capital | (III) Wages | | (D) Entrepreneurship | (IV) Rent | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Parallel inward shift in budget line | (I) M/p₁ > M/p₁' | | (B) Parallel outward shift in budget line | (II) M/p₁ < M/p₁' | | (C) Budget line steeper | (III) M' < M | | (D) Budget line flatter | (IV) M' > M | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) The minimum level of profit that is needed to keep a firm in the existing business. | (I) Super-normal profit | | (B) Profit that a firm earns over and above the normal profit. | (II) Loss | | (C) AR < AC | (III) Break even point | | (D) The point of minimum average cost at which the supply curve cuts the AC curve. | (IV) Normal Profit | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Leftward shift in both the supply and demand curve | (I) Equilibrium price remains unchanged | | (B) Rightward shift in both supply and demand curve | (II) Equilibrium quantity increases | | (C) Equal percentage of increase in both demand and supply curves | (III) Equilibrium quantity decreases | | (D) Shifts in supply curve towards right and demand curve shifts left | (IV) Equilibrium quantity remains unchanged | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Substitution effect stronger than the income effect | (I) Inferior goods | | (B) Income effect stronger than the substitution effect | (II) Complementary goods | | (C) Demands and income move opposite direction | (III) Normal goods | | (D) Goods consumed together | (IV) Giffen goods | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Control Price | (I) Set below the equilibrium price | | (B) Floor Price | (II) Fixed by the government for the labourers | | (C) Minimum Wage Legislation | (III) Set above the equilibrium price | | (D) Market Equilibrium | (IV) when demand and supply curve intersect. | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Budget line | (I) $-\frac{p_1}{p_2}$ | | (B) Budget constraint | (II) Bundles available to the consumer | | (C) Budget set | (III) $p_1X_1 + p_2X_2 = M$ | | (D) Slope of budget line | (IV) $p_1X_1 + p_2X_2 \leq M$ | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Marginal rate of substitution | (I) Slope of Budget line | | (B) MUₓ/MUᵧ=Pₓ/Pᵧ | (II) more of at least one good and no less of the other good | | (C) -(Pₓ/Pᵧ) | (III) Law of equi marginal utility | | (D)Monotonic Preferences. | (IV) Slope of Indifference curve | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Demand and supply curve shift leftward | (I) Quantity may increase, decrease or remain unchanged and price decreases | | (B) Demand and supply curve shift rightward | (II) Quantity may increase, decrease or remain unchanged and price increases | | (C) Demand curve shifts leftward and supply curve rightward | (III) Quantity decreases and price may increase, decrease or remain unchanged | | (D) Demand curve shifts rightward and supply curve leftward | (IV) Quantity increases and prices may increase, decrease or remain unchanged | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Production function | (I) $x_1^α x_2^β$ | | (B) Constant return to scale | (II) $α + β = 1$ | | (C) Increasing return to scale | (III) $α + β < 1$ | | (D) Decreasing return to scale | (IV) $α + β > 1$ | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Price elasticity of demand will be equal to1 | (I) When expenditure increases with a rise in price. | | (B) Price elasticity of demand will be equal to 0 | (II) When expenditure decreases with a rise in price. | | (C) Price elasticity of demand will be more than 1 | (III) When the quantity demanded doesn't change with the change in price. | | (D) Price elasticity of demand will be less than1 | (IV) When expenditure doesn't change with the change in price. | Choose the correct answer from the options given below: 1. (A) - (I), (B) - (II), (C) - (III), (D) - (IV) 2. (A) - (III), (B) - (IV), (C) - (II), (D) - (I) 3. (A) - (IV), (B) - (III), (C) - (II), (D) - (I) 4. (A) - (IV), (B) - (III), (C) - (I), (D) - (II)

Match List-I with List-II | List-I | List-II | |---|---| | (A) Slope of Budget line | (I) $P_1X_1 + P_2X_2 \leq M$ | | (B) Horizontal intercept of budget line | (II) $M/P_2$ | | (C) Vertical intercept of budget line | (III) $-\frac{P_1}{P_2}$ | | (D) Budget constraints | (IV) $M/P_1$ | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Normal profit | (I) Minimum level of profit need by firm to be in business. | | (B) Shut down point | (II) Minimum level of LRAC curve | | (C) Break-even point | (III) Profit Over and above normal profit | | (D) Super-normal profit | (IV) The point on which firm earn only normal profit. | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Decrease in consumer's income | (I) Budget line becomes steeper | | (B) Increase in price of Good X | (II) Parallel and leftward shift in the budget line | | (C) Equal reduction in price of both goods X and Y | (III) Budget line becomes flatter | | (D) Increase in price of Good Y | (IV) No change in the slope of the budget line | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) TVC | (I) AVC × quantity | | (B) SAC | (II) AVC + AFC | | (C) TC | (III) TVC + TFC | | (D) LRMC | (IV) (TC at q₁ units) – (TC at q₁ – ₁ units) | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Increase in demand > Increase in Supply | (I) Increase in both equilibrium price and quantity. | | (B) Increase in demand < Increase in Supply | (II) Decrease in both equilibrium price and quantity. | | (C) Increase in demand = Increase in Supply | (III) Decrease in equilibrium price but increase in equilibrium quantity. | | (D) Decrease in demand < Decrease in supply | (IV) Increase in equilibrium quantity but no change in equilibrium price. | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A). The level of utility can be expressed in numbers. | (I). Total Utility | | (B). The change in total utility due to consumption of one additional unit of a commodity. | (II). Ordinal Utility | | (C). The total satisfaction derived from consuming the given amount of some commodity. | (III). Cardinal Utility | | (D). The level of utility can be expressed in ranks. | (IV). Marginal Utility | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Demand shifts right and supply remains unchanged. | (I) Price increase, quantity increases. | | (B) Supply shifts right and demand remains unchanged. | (II) Price decrease, quantity increases. | | (C) Demand shifts left and supply shifts left. | (III) Quantity decreases. | | (D) Supply shifts right and demand shifts right. | (IV) Quantity increases. | Choose the correct answer from the options given below: 1. (A) - (I), (B) - (II), (C) - (III), (D) - (IV) 2. (A) - (II), (B) - (I), (C) - (III), (D) - (IV) 3. (A) - (I), (B) - (II), (C) - (IV), (D) - (III) 4. (A) - (III), (B) - (IV), (C) - (I), (D) - (II)

Match List-I with List-II | List-I | List-II | |---|---| | (A) Excess demand | (I) Supernormal profits | | (B) Excess supply | (II) Perfect competition | | (C) Entry of new firms in the market | (III) Price tends to fall | | (D) Price taker | (IV) Price tends to rise | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Perfect Competition | (I) No change in equilibrium price | | (B) Increase in Demand= Decrease in Supply | (II) Price taking Behavior | | (C) Increase in Demand > Decrease in Supply | (III) Decrease in equilibrium price | | (D) Increase in Supply > Decrease in Demand | (IV) Increase in equilibrium price | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Increase in price of goods X | (I) Increase in demand for normal goods. | | (B) Increase in income of consumers | (II) Demand is price inelastic | | (C) Good X is a necessary good | (III) Unit elasticity of demand. | | (D) Demand curve of Good X is a rectangular hyperbola | (IV) Contraction in demand for good X | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Consumer's income changes, but prices remain unchanged. The equation of the budget line. | (I) p₁ x₁ + p₂ x₂ = M' | | (B) Marginal Rate of Substitution (MRS) | (II) p'₁ x₁ + p₂ x₂ = M | | (C) The price of a commodity changes, but income remains unchanged. The equation of the budget line. | (III) Δ Y/ΔX | | (D) Total Utility | (IV) $MU₁ + MU₂ + ... + MU_{n-1} + MU_n$ | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Total Cost | (I) Change in total cost when an additional unit of output is produced. | | (B) Marginal Cost | (II) Vertical summation of Average Fixed Cost (AFC) and Average Variable Cost (AVC) curves. | | (C) Fixed Cost | (III) Explicit Costs + Implicit Costs. | | (D) Short period Average Cost (AC) Curve | (IV) Does not change with increase or decrease in output. | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Short run Marginal Cost (SMC) | (I) ΔTC/Δq | | (B) Long run Average Cost (LRAC) | (II) TVC/q | | (C) Average Variable Cost (AVC) | (III) TC/q | | (D) Average Fixed cost (AFC) | (IV) TFC/q | Choose the correct answer from the options given below:

Match List-I with List-II | List-I | List-II | |---|---| | (A) Increase in consumers' income | (I) Budget line becomes flatter | | (B) Decrease in price of good on X axis | (II) No change in the slope of budget line | | (C) Equal increase in price of both good X and good Y | (III) Parallel and rightward shift in their budget line | | (D) Decrease in Price of the good on Y axis | (IV) Budget line becomes steeper | Choose the correct answer from the options given below:

Match List-I with List-II | List–I | List–II | | ----------------------- | -------------------------------------- | | (A) Total variable cost | (I) TR – (TVC + TFC) | | (B) Total Revenue | (II) TVCₙ – TVCₙ₋₁ | | (C) Profit | (III) Average variable cost × Quantity | | (D) Marginal cost | (IV) Price × Quantity | Choose the correct answer from the options given below:

Match List-I with List-II | List–I | List–II | | ---------------------------------------------------------------------------------------------------- | --------------------------------- | | (A) A proportional increase in all inputs results in an increase in output by a smaller proportion | (I) Constant returns to scale | | (B) A proportional increase in all inputs results in an increase in output by a larger proportion | (II) Law of variable proportions | | (C) A proportional increase in all inputs results in an increase in output by the same proportion | (III) Decreasing Returns to Scale | | (D) Factor proportions change as long as one factor is held constant and the other factors increases | (IV) Increasing Returns to Scale | Choose the correct answer from the options given below:

Match List-I with List-II (TP : TOTAL PRODUCT; L: UNITS OF LABOUR) | List-I | List-II | |---|---| | (A) $TP/L$ | (I) Total Product is maximum | | (B) $\Delta TP/\Delta L$ | (II) Marginal product | | (C) $\sum MP$ | (III) Total product | | (D) $MP=0$ | (IV) Average Product | Choose the correct answer from the options given below:

Minimum support price of a foodgrain is the example of _______

________ of an input is defined as the change in output per unit of change in the input when all other inputs are remain constant.

On the basis of given data above, the correct equation of price line will be.

On the basis of given data, the slope of the price line will be _________

Perfect information implies that all buyers and all sellers are completely informed about the price, quality and other relevant details about the product, as well as the market. These features result in the single most distinguishing characteristic of perfect competition, that is...

Positive Economics deals with_______________

Price ceiling is one concept which provides safeguard to______

Price ceilings are also known as............

Public goods, as distinct from private goods, are collectively consumed. Two important features of public goods are:

Select the correct statements from the following with regard to cost curves : (A) Short run marginal cost, average variable cost and short run average cost curves are 'U'-shaped. (B) SMC curve cuts the AVC curve from below at the minimum point of AVC. (C) SMC curve cuts the AFC curve from below at the minimum point of AFC. (D) Average fixed cost curve is downward sloping. Choose the correct answer from the options given below:

Select the INCORRECT condition for profit maximisation in the perfect market. 1. The price must equal to MC. 2. Marginal cost must be non-decreasing. 3. Price must be less than the average cost. 4. Price must be greater than the average cost.

Select the INCORRECT feature of the market with respect to perfect competition. 1. The market consists of a large number of buyers and sellers. 2. Entry into the market as well as exit from the market are free for firms. 3. Buyers are price makers. 4. There is perfect knowledge.

Set of all possible combinations of the two inputs that yield the same maximum possible level of output is known as.........

Shape of Average Fixed Cost Curve is:

Stages of production are the consequences of:

Suppose a consumer purchase 15 bananas when its price is Rs. 5 per banana. When the price increases to Rs. 7 per banana, consumer reduces his demand to 12 bananas. Price elasticity of demand would be........... 1. 0.5 2. 0.6 3. 0.4 4. 0.7

Suppose an individual buy 30 bananas when its price is Rs. 10 per banana. When the price increases to Rs. 14 per banana, she reduces her demand to 24 bananas. In this case,what will be the price elasticity of demand?

suppose an individual with same working condition got three alternative job in his hand he has selected the best and need to forgone the next best alternative. Identify the indicated cost in the aforesaid statement.

Suppose in a production process, all inputs get doubled. As a result, if the output gets doubled, the production function exhibits? 1. Decreasing Return to scale. 2. Incresing Returns to scale. 3. Constant Return to scale. 4. Decresing Productivity.

Suppose in the long run, the government imposed a tax on the supply of a commodity. How does it affect the equilibrium quantity of commodity? 1. The quantity of commodity will decrease. 2. The quantity of commodity will increase. 3. The quantity of commodity will remain same. 4. The supply curve will shift rightwards which will decrease quantity of commodity.

Suppose that the unit tax imposed by the government is Rs 50. Then, if the firm produces and sells 100 units of the good, the total tax that the firm must pay to the government is ...................

Suppose the demand and supply curves of salt are given by: $Q_d = 1000 - p$ $Q_s = 700 + 2p$ Find the equilibrium price and quantity.

Suppose the Income of consumers in a market increase. How will this effect the equilibrium price of the commodity, assuming that it is a normal good? (A) There is excess demand at the existing price. (B) Rising price leads to contraction in demand and expansion in supply and a new equilibrium price is attained, which is higher than the initial price. (C) The demand curve shifts rightward. (D) There is upward pressure on the price and price starts rising. Choose the correct answer from the options given below:

Suppose the market determined rent for apartments is \$200 per month. The government intervenes and sets the rent control at $250 per month. What is the likely impact of this intervention on market of apartments?

The allocation of scarce resources and the distribution of the final goods and services are the _____ of any economy. 1. States problems 2. Consumption problems 3. Central problems 4. Production problems

The book 'An Enquiry into the Nature and Cause of the Wealth of Nations' was published in which of the following year.

The book 'An Enquiry into the Nature and Causes of the Wealth of Nations' is written by: 1. J. M. Keynes 2. David Ricardo 3. Adam Smith 4. Karl Marx

The case where a marginal product is greater than the average product, where? 1. MP cut AP at Minimum 2. AP remains Constant 3. AP Decreases 4. AP Increases

The change in output per unit of change in the input when all other inputs are held constant, is termed as __________.

The change in total cost per unit of change in output is known as by which name

The collection of all possible combinations of goods and services that can be produced from a given amount of resources and a given stock of technological knowledge.

The collection of all possible combinations of the goods and services that can be produced from a given amount of resources and a given stock of technological knowledge is called?

The core reason behind the arising law of proportion is............ 1. Factor proportion changes with keeping one factor constant. 2. Decrease in all input. 3. Increase in all input. 4. All factors remain constant.

The cost of a firm has increased from Rs. $67$ to Rs. $80$ when the units of cotton production rose from $8$ to $9$. Calculate the marginal cost of a firm?

The curve gives the maximum amount of corn that can be produced in the economy for any given amount of cotton and vice versa. This curve is called.........

The demand curve that a firm faces in a perfectly competitive market is...........

The difference between the revenue and cost is known as________

The economic approach in which we try to understand whether given mechanisms are desirable or not is known as ..........

The economic concept at which the consumer is willing to substitute one good for the other?

The equation of demand curve of a good for a consumer is given to be $p_d = e$ where e is a constant. What will be the shape of the demand curve?

The equation of long-run marginal cost.

The equation of the demand curve : pq = e, where e is a constant. Select the INCORRECT statement: 1. The demand curve is a rectangular hyperbola. 2. The value of p times q is constant. 3. The elasticity of demand at all points located on this demand curve is greater than 1. 4. At every point of consumption, the expenditure remains the same.

The exceptional case in optimal choice of the consumer is where ..................

The existence of a large number of buyers and sellers in the perfectly competitive market means?

The firm must employ more of the variable inputs, in order to increase the production of output. Therefore, as output increases

The first book on Microeconomics, "An inquiry into Nature and Cause of the Wealth of Nations", was written by_________.

The government-imposed lower limit on the price that may be charged for a particular good or service. What this lower limit is called ?

The income of a consumer is spent by him on two goods X and Y. The marginal utility of the goods at the present level of consumption are equal to each other. However, the price of good X is double that of good Y. The consumer, in order to attain equilibrium, will

The Law of Diminishing Marginal Utility states that when more and more units of a commodity are consumed, Marginal Utility __________

The marginal product of an input initially rises and then after a certain level of employment, it starts falling, thus MP curve looks like an inverse 'U'- shaped curve. This condition is under ............

The market determined price of a good is Rs. 40.The government fixes the minimum price of the good as Rs. 50. Calculate the excess demand/excess supply it will cause if the demand and supply functions are Qd = 200 – p and Qs = 120 + p respectively.

The market determined price of a good is Rs. 40.The government determines the price ceiling on the good as Rs. 25. Calculate the excess demand/excess supply it will cause if the demand and supply functions are Qd= 200 – p and Qs=120+ p respectively.

The market determined wage rate is \$500 per month whereas the minimum wage fixed by the government is $\$450 per month. As a result of this government intervention,

The optimum bundle of the consumer is located at the point where:

The optimum bundle of the consumer is located at the point where..................?

The optimum output will be when the relationship between LRMC and LRAC.

The point of minimum average cost at which the supply curve cuts the long run average cost curve is called?

The point on the supply curve at which a firm earns only normal profit is called ...........

The price and quantity demanded are __________

The price elasticity of demand is different at different points on the linear demand curve. Arrange the elasticity point on a downward sloping (left to right) demand curve. (A). |ed| < 0 (B). |ed| = 1 (C). |ed| > 1 (D). |ed| < 1 Choose the correct answer from the options given below:

The price elasticity of supply of a commodity is 2.5. At a price of Rs.5 per unit, its quantity supplied is 300 units. What will be its quantity supplied at a price of Rs.4 per unit?

The price of a commodity increases by 10%, its demand drops by 12%. What is the nature of price elasticity of demand?

The problem 'For whom to produce' is basically concerned with _______.

The problem of 'what to produce' relates to?

The q (1 + e_p) < 0, and hence, ΔE (expenditure) has the opposite sign as Δp (price), if ...................

The rate at which consumer is willing to substitute one good for another is represented by ________.

The rate at which the consumer is able to substitute one good for the other in the market is called?

The rate at which the consumer is able to substitute one good for the other in the market is indicated by

The rate at which the consumer is willing to substitute one good for the other is indicated by:

The relation between the consumer's optimal choice of the quantity of a good and its price is called ?

The relationship between an increase in variable input and output when all other inputs are held constant is referred to as.

The relationship between inputs and outputs of a firm is given by ___________

The scarcity of resources in the economy gives rise to the problem of............

The set of all possible combinations of the two inputs that yield the same maximum possible level of output is known as...........

The set of all possible combinations of the two inputs, labour and capital, that yield the same maximum possible level of output is called...........

The shape of the average fixed cost curve is ........................

The shape of the average product and marginal product curves are................... 1. Both Inverse 'U' Shaped 2. Both 'U' Shaped 3. AP 'U' Shaped and MP Inverse 'U' Shaped 4. MP 'U' Shaped and AP Inverse 'U' shaped

The shape of the long-run average cost curve and long-run marginal cost curve.

The short run supply curve is represented as? 1. The rising part of the marginal cost curve. 2. The rising part of the marginal cost curve from and above the minimum average variable cost curve. 3. The rising part of the marginal cost curve from and above the minimum average cost curve. 4. The marginal cost curve.

The slope of Production Possibility curve is represented by ___________.

The tendency where marginal productivity first increases then starts falling is known as ______

The total cost is equal to Rs.95 for 7 units of output and Rs.115 for 8 units of output. What is the marginal cost at the quantity of 8th unit?

The total cost of a firm is Rs 80 for 3 units of output, Rs 95 for 4 units of output, and Rs. 115 for 5 units of output. What is the marginal cost for the 5th unit of output?

The total revenue of a firm is increasing at a constant rate. Which of the following is true about this firm?

The total satisfaction derived from consuming the given amount of commodity X is known as _______

The total sum consumer spends on cloth in 2022?

The total sum consumer will spends on cloth in 2025?

The total sum that the consumer has to spend on wheat in 2022?

The total sum that the consumer has to spend on wheat in 2025?

The wage rate at which the labour market is in equilibrium is a point where. 1. Labour demand=0 2. Labour Demand= Labour Supply 3. Labour Supply=Labour Demand=0 4. Wages= Marginal Revenue from labour x Price

There are two goods that are priced at Rs 5 each and are available only in integral units. If a consumer has Rs 20, then the bundle that this consumer can afford to buy is:

To be effective, the floor price should be determined

To increase the output by a certain proportion, if inputs need to be increased by more than that proportion, that condition lies in which of the following?

Two goods X and Y are such a combination that, when the price of good Y increases, the demand for good X increases, How are goods X and Y related?

Two indifference curves can never intersect each other as ............... 1. They give the same level of satisfaction. 2. They give different levels of satisfaction. 3. They are concave to the origin. 4. They are convex to the origin.

Under perfect competition, for the producer to be in equilibrium:

Under perfect competition if firms earn supernormal profits. Arrange following statements to arrive at the implication of free entry and exit of firms (A) Market price fall in such a manner that firms will be earning normal profits only and thus no more firms will have incentive to enter the market. (B) Some new firms will enter the market (C) At the prevailing market price, each firm is earning supernormal profit. (D) Demand remains unchanged but the market supply curve shifts rightward

What are the features of an Indifference Curve? (A) Indifference curve slopes upwards from left to right. (B) Higher indifference curve gives greater level of utility. (C) Indifference curve slopes downwards from left to right (D) Two indifference curves never intersect each other Choose the correct answer from the options given below:

What are the key components of a perfectly competitive market? (A) Large number of buyers and sellers. (B) Homogeneous product. (C) Free Entry and exit. (D) Asymmetric Information. Choose the correct answer from the options given below:

What causes an indifference curve to be convex to the origin? 1. Marginal utility 2. Market Rate of Exchange 3. Law of Diminishing Marginal Rate of Substitution 4. Law of Increasing Marginal Rate of Substitution

What does break even point indicate?

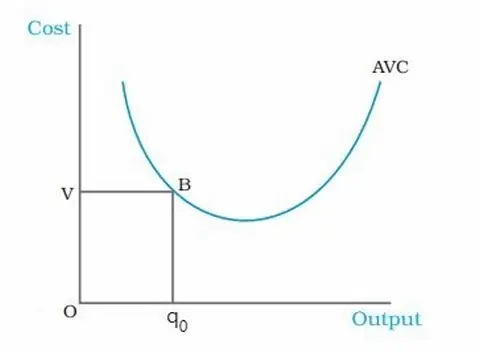

What does the rectangle OVBq₀ depicts in the given figure?

What is Consumer Price Index?

What is the fixed cost for producing 200 vases?

What is the formula for the price elasticity of demand for a good?

What is the main purpose of Cost Reduction Technologies in business?

What is the Marginal Rate of Substitution(MRS)? (A) The rate at which a consumer is willing to substitute one good for another. (B) Equal to the slope of the indifference curve. (C) Changes as we move along the indifference curve. (D) Is constant for perfect substitutes. Choose the correct answer from the options given below:

What is the shape of Average Revenue (AR) curve under perfect competition?

What is the total variable cost for producing 200 vases?

What will be elasticity of demand of a commodity when its price rises by 20% and quantity demanded falls from 125 units to 75 units?

What will be the average variable cost (AVC) for producing 200 vases?

What will be the shape of unitary elastic supply curve?

What will be the value of Marginal utility of the 4th unit | Units consumed | Total Utility derived (utils) | |---|---| | 1 | 10 | | 2 | 8 | | 3 | 5 | | 4 | 2 |

What would be the equilibrium number of firms in a market of identical firms, when market demand function $(Q_d)$, supply function of a single firm $(Q_s1)$ and equilibrium price (P) are given as $Q_d = 180 - 2P$ $Q_{s1} = 15 + P$ $P = 15$ 1. 5 2. 6 3. 8 4. 9

What would be the value of the Marginal Rate of Substitution (MRS) when Good-X increases by 5 with the decrease of Good-Y by 15?

What would price ceiling lead to when the maximum price is fixed lower than the equilibrium price?

When a firm increases its output and the average cost rises, this phase in the production process is shown as?

When both the demand and supply curves shift to indicate an increase in demand and supply in the same proportion. Then:

When demand curve shift rightward and supply curve shift leftward what impact this will have on pricing?

When Government fix the minimum price of any commodity this move of government is known by:

When in an economy, available resources are fully utilized at that point production of a combination of goods is known as .........

When labor changes from 3 to 4, the total product changes from 24 to 40, calculate the marginal product.

When Marginal Product is constant?

When Marginal productivity starts decreasing but remains positive , Total Productivity is ______.

When more and more workers are applied on the fixed land then the marginal productivity of additional worker will ............... to the total output.

When more workers are hired, the land begins to get 'crowded'. Each worker now has insufficient land to work efficiently. So the output added by each additional worker is now proportionally less as a result the marginal product begins to __________.

When output increases with smaller proportion compare to increase in inputs, this return is called? 1. Decreasing Return to scale 2. Increasing Return to scale. 3. Constant Return to scale. 4. Incremental Productivity.

When output increases with the larger proportion compare to increase in inputs, this return is called? 1. Decreasing Return to scale. 2. Increasing return to scale. 3. Constant Return to scale. 4. Diminishing Marginal Product.

When output increases with the same proportion as increase in inputs, this concept is known by? 1. Marginal diminishing returns. 2. Decreasing return to scale. 3. Increasing return to scale. 4. Constant Return to scale.

When some resources are shifted from Use 1 to Use 2 (given technology), the Marginal Rate of Transformation will

When the additional unit of input is 'crowded' in the production, the output is proportionally less and............

When the average cost is rising, then.

When the output added by each additional worker is proportionally less, what it shows?

When the output is zero in the short run. Which of the following costs are undefined?

When the percentage change in quantity demanded equals the percentage change in its price. The demand for the this good is said to be? - Perfectly Elastic - Perfectlty Inelastic - Unitary Elastic - Less Elastic

When the price elasticity of supply is equal to zero. Then.......... 1. Supply curve is sloping downward. 2. Supply curve is horizontal. 3. Supply curve is upwards sloping. 4. Supply curve is vertical.

When the price of a cricket ball is Rs10, let us assume that 200 cricket balls are produced in aggregate by the firms in the market. When the price of a cricket ball rises to Rs.30, let us assume that 1,000 cricket balls are produced in aggregate by the firms in the market. Calculate the elasticity of supply.

When utility is measured in quantitative terms, it is ______ of consumer equilibrium.

When we have proportionately more output than input this economic concept is known as .........

When will increase in supply bring down the price, leaving the quantity demanded unchanged?

Whether to have more consumption goods or to have investment goods which will boost production and consumption tomorrow, is a part of which of the central problem?

Whether to use more resources in education and health or to use more resources in building military services. Which of the central problems of an economy is accurate for this?